Standard loans are frequently also "conforming loans," which indicates they meet a set of requirements specified by Fannie Mae and Freddie Mac 2 government-sponsored enterprises that buy loans from loan providers so they can provide home loans to more individuals. Traditional loans are a popular option for purchasers. You can get a conventional loan with as little as 3% down.

This contributes to your monthly expenses but enables you to enter a new home quicker. USDA loans are only for homes in qualified backwoods (although numerous houses in the suburbs certify as "rural" according to the USDA's definition.). To get a USDA loan, your home income can't go beyond 115% of the area average income.

For some, the warranty fees needed by the USDA program expense less than the FHA mortgage insurance coverage premium. VA loans are for active-duty military members and veterans. how do uk mortgages work. Backed by the Department of Veterans Affairs, VA loans are an advantage of service for those who have actually served our nation. VA loans are an excellent option due to the fact that they let you purchase a house with 0% down and no personal mortgage insurance.

Each month-to-month payment has four significant parts: principal, interest, taxes and insurance coverage. Your loan principal is the quantity of cash you have actually delegated pay on the loan. For instance, if you borrow $200,000 to buy a home and you settle $10,000, your principal is $190,000. Part of your monthly mortgage payment will automatically approach paying for your principal.

Some Known Factual Statements About How Do 2nd Mortgages Work?

The interest you pay every month is based upon your rates of interest and loan principal. The cash you pay for interest goes directly to your mortgage provider. As your loan matures, you pay less in interest as your primary reductions. If your loan has an escrow account, your regular monthly home loan payment may likewise consist of payments for real estate tax and house owners insurance coverage.

Then, when your taxes or insurance premiums are due, your lender will pay those expenses for you. Your home loan term describes for how long you'll pay on your home loan. The two most common terms are 30 years and 15 years. A longer term usually implies lower regular monthly payments. A much shorter term typically indicates bigger monthly payments however big interest cost savings.

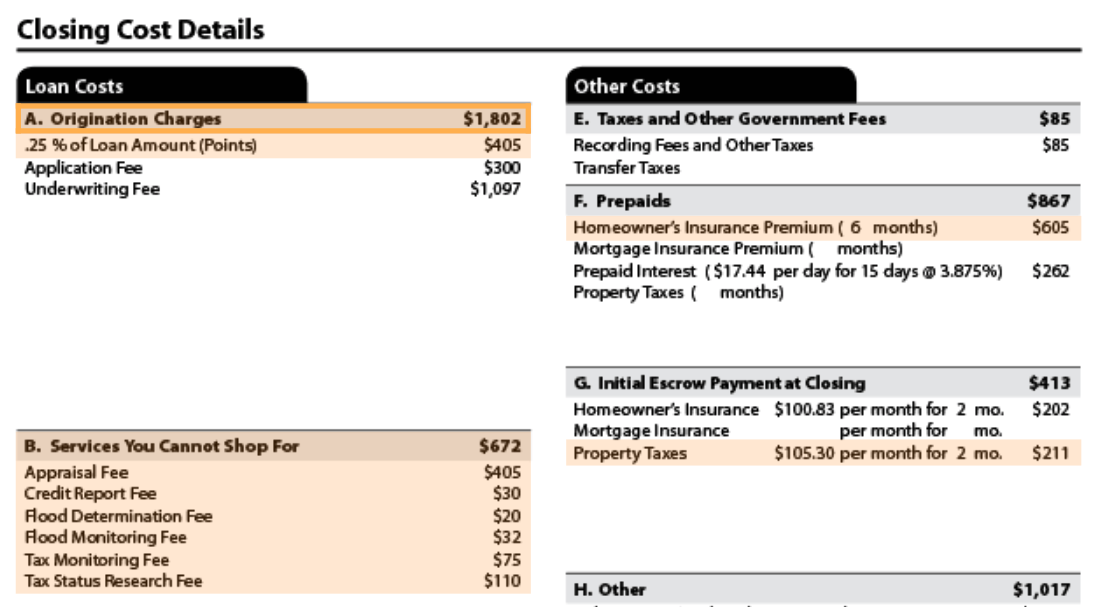

Most of the times, you'll require to pay PMI if your deposit is less than 20%. The cost of PMI can be included to your monthly home mortgage payment, covered by means of a one-time upfront payment at closing or a combination of both. There's likewise a lender-paid PMI, in which you pay a slightly higher rates of interest on the home mortgage instead of paying the regular monthly cost.

It is the composed pledge or arrangement to repay the loan utilizing the agreed-upon terms. These terms consist of: Interest rate type (adjustable or repaired) Rates of interest portion Quantity of time to pay back the loan (loan term) Amount borrowed to be repaid completely Once the loan is paid in full, the promissory note is offered back to the borrower.

The Definitive Guide for How Do Dutch Mortgages Work

The American dream is the belief that, through hard work, nerve, and decision, each individual can achieve financial prosperity. A lot of individuals analyze this to suggest an effective profession, status seeking, and owning a home, a cars and truck, and a family with 2. 5 children and a pet dog. The core of this dream is based on owning a house.

A home loan is simply a long-term loan given by a bank or other financing institution that is protected by a specific piece of property. If you fail to make timely payments, the lender can reclaim the home. Due to the fact that houses tend to be costly - as are the loans to spend for them - banks permit you to repay them over extended durations of time, called the "term".

Shorter terms might have lower interest rates than their similar long-lasting siblings. However, longer-term loans may offer the benefit of having lower monthly payments, because you're taking more time to pay off the debt. In the old days, a close-by cost savings and loan might provide you cash http://riverzaqp779.lowescouponn.com/what-does-how-d-mortgages-work-mean to purchase your house if it had adequate money lying around from its deposits.

The bank that holds your loan is responsible mainly for "servicing" it. When you have a mortgage, your month-to-month payment will usually consist of the following: A quantity for the principal amount of the balance An amount for interest owed on that balance Real estate taxes Homeowner's insurance coverage Home Home mortgage interest rates can be found in a number of ranges.

How Does Point Work In Mortgages for Beginners

With an "adjustable rate" the rates of interest changes based on a specified index. As an outcome, your monthly payment amount will change. Home mortgage loans can be found in a range of types, consisting of conventional, non-conventional, set and variable-rate, house equity loans, interest-only and reverse home loans. At Mortgageloan. com, we can assist make this part of your American dream as easy as apple pie.

Most likely one of the most confusing things about home mortgages and other loans is the estimation of interest. With variations in intensifying, terms and other aspects, it's tough to compare apples to apples when comparing home loans. In some cases it looks like we're comparing apples to grapefruits. For example, what if you desire to compare a 30-year fixed-rate mortgage at 7 percent with one indicate a 15-year fixed-rate mortgage at 6 percent with one-and-a-half points? Initially, you have to keep in mind to also consider the charges and other expenses connected with each loan.

Lenders are needed by the Federal Truth in Loaning Act to divulge the effective percentage rate, as well as the total financing charge in dollars. Advertisement The annual percentage rate () that you hear a lot about allows you to make true comparisons of the actual expenses of loans. The APR is the average yearly financing charge (that includes charges and other loan costs) divided by the quantity borrowed.

The APR will be a little greater than the interest rate the lending institution is charging because it includes all (or most) of the other costs that the loan brings with it, such as the origination fee, points and PMI premiums. Here's an example of how the APR works. You see an ad providing a 30-year fixed-rate home loan at 7 percent with one point.

The Single Strategy To Use For How Does Securitization Of Mortgages Work

Easy option, right? Actually, it isn't. Luckily, the APR considers all of the small print. Say you need to borrow $100,000. With either lender, that implies that your month-to-month payment is $665. 30. If the point is 1 percent of $100,000 ($ 1,000), the application fee is $25, the processing charge is $250, and the other closing charges amount to $750, then the total of those costs ($ 2,025) is subtracted from the real loan quantity of $100,000 ($ 100,000 - $2,025 = $97,975).

To discover the APR, you identify the rates of interest that would relate to a month-to-month payment of $665. 30 for a loan of $97,975. In this case, it's actually 7. 2 percent. So the 2nd loan provider is the better deal, right? Not so quick. Keep checking out to learn more about the relation in between APR and origination fees.