Here are trends we see on the horizon in the upcoming month and year. Though everybody believed COVID-19 would be a distant memory by the fall of 2020, it will still be altering nearly every part of life well into 2021. Cases will continue to rise, implying more lockdowns, quarantines, and social distancing throughout the U.S.

According to CNN, 110,000 restaurants have completely closed in 2020 17% of the U.S. overall. Significant employers like airline companies and cruise lines, plus numerous small companies, are likewise teetering toward insolvency. Just one thing is specific: financial recovery won't take place over night. And in unsure economic times, home mortgage rates do stunningly well.

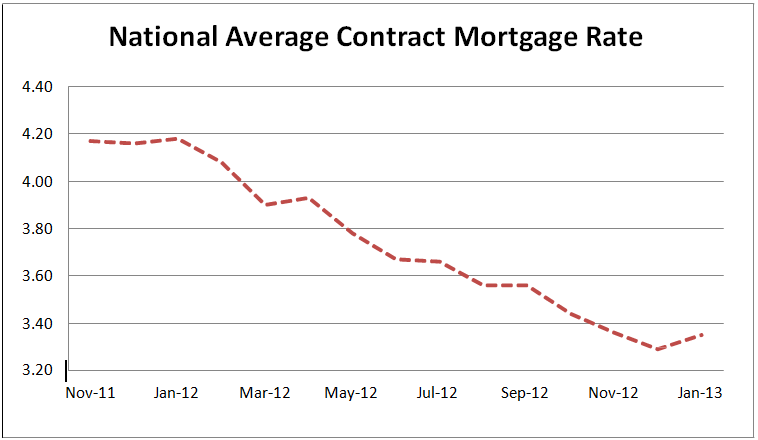

But what about the Fannie Mae "refinance charge"? Lots of in the industry believed the charge, enforced December 1, would immediately add 0. timeshare exchanges companies 125% to most refinances. That just didn't happen - what to know about mortgages in canada. In reality, Freddie Mac reported an all-time-low 30-year fixed rate of 2. 71% throughout the week of December 10, long after lending institutions timeshare angels started enforcing the cost.

In reality, many lenders are offering rates greater than they need to. They do this so they can slow income applications and procedure existing ones without enormous delays and customer service fails. As constantly, look around with multiple lenders to get your least expensive rate. Record-low rates are still out there, regardless of the "refinance fee." The Federal Reserve will do what it can to keep rates low.

5 Easy Facts About How Do Mortgages Work In The Us Shown

The Fed meets again on January 26-27, 2021. A lot of experts expect the exact same "loose money" stance it has taken because the break out of the infection. The rate-friendly position is an advantage for home mortgage shoppers. While the Fed does not impact home loan rates directly, its belief permeates the whole economy consisting of rates of interest of all kinds.

Up until recently, it focused greatly on keeping inflation in check. While that's still its mandate, it now puts more focus on propping up the economy in this time of pressure. The Federal Reserve wants to let its policies drive inflation above its 2 percent objective for prolonged periods a break from its previous method.

The group has transformed from an inflation-fearing body to a recession-fearing one. What does this mean for the personal finances of the average American customer? It indicates you'll likely have access to ultra-low rates for years. Possibly not as low as they are now, however extremely low from a historical viewpoint.

Housing agencies across the country are requiring rates in the high 2s and low 3s for 2021. 2. 80% 2. 89% 3. 00% 3. 00% 3. 20% 3. 30% To sum it up, rate forecasts differ extensively. Today's rate may be as great as we'll see for several years to come, or they might enhance.

A Biased View of How Many Mortgages Can One Person Have

Each year, federal government firms examine rate increases throughout the country to determine loan amount caps for its standard and FHA loans. Here are the numbers for 2021: 1-unit houses: $548,2502-unit houses: $702,0003-unit houses: $848,5004-unit houses: $1,054,500 1-unit houses: $356,3622-unit houses: $456,2753-unit houses: $551,5004-unit houses: $685,400 These are limitations in low- to average-cost locations.

This is substantial for some home purchasers because it means they can avoid the stricter guidelines that include jumbo loans. State a house purchaser is purchasing a $1 million house with $180,000 down in Los Angeles. They now certify for a conforming loan, considering that $820,000 is within the limitations for that area.

If you believed you were going to require a jumbo loan, run the numbers again with brand-new, greater 2021 loan limits. You may be shocked. If you still need a jumbo loan, even at the higher 2021 mortgage limits, consider a piggyback loan. That's where you include a 2nd home mortgage on top of your very first home mortgage.

How? Here's an example. Purchase rate $1 millionLocal loan limit: $700,000 Down payment $200,000 Here are the alternatives in this situation: Option 1: One jumbo loan at $800,000 Alternative 2: Conforming loan at $700,000 plus a second home loan for $100,000 You might select Choice 2 if you can't quite get approved for a jumbo loan due to its greater standards for credit and readily available properties.

Rumored Buzz on What Percentage Of Mortgages Are Fha

The two-loan solution will be a widely-used tool in 2021 as house rates warm up under restored competitors for homes. Home worths increased in 2020. As we enter 2021, homeowners will take pleasure in the double blessing of rising house worths and low rates. This puts them in a great position to refinance out of mortgage insurance.

The average is more like 6%. But that means most novice home purchasers are paying some sort of home loan insurance. Mortgage insurance is okay, but it's not fun to pay, either. Fortunately, numerous house owners now have 20% equity in spite of putting just 5-10% down not that long earlier. These homeowners can refinance into a conventional loan and get rid of home loan insurance coverage altogether.

It could conserve you hundreds of dollars each month. If your house equity has actually skyrocketed in the last 12-24 months, it deserves talking with a lending institution, who can let you understand your chances of re-financing out of your home loan insurance coverage for excellent. Numerous home mortgage consumers do not recognize there are several kinds of rates in today's home mortgage market.

Following are updates for specific loan types and their corresponding rates - what are the lowest interest rates for mortgages. Conventional re-finance rates and those for home purchases have actually trended lower in 2020. According to loan software application business Ellie Mae, the 30-year home mortgage rate balanced 3. 01% in October (the most recent data readily available), down from 3. 02% in September.

Get This Report on What Is Required Down Payment On Mortgages

71% weekly average due to the fact that it consider low credit and low-down-payment traditional loan closings, which tend to come with greater rates. Plus, it's a more postponed report, and rate of interest have been dropping. Lower credit report customers can use standard loans, however these loans are more fit for those with good credit and a minimum of 3 percent down.

Twenty percent of equity is preferred when refinancing. With sufficient equity in the house, a traditional refinance can settle any loan type. Got an Alt-A, subprime, or high-PMI loan? A standard refi can look after it. For circumstances, state you bought a home 3 years ago with an FHA loan at 3.

Given that then, home costs have increased. Due to the fact that of your greater home worth, you now have 20 percent equity, which suggests you could refinance into a traditional loan and remove FHA mortgage insurance. This might be a savings of hundreds of dollars per month, Eliminating home mortgage insurance is a big deal in any home mortgage market.

Get in a 20 percent down payment to see your new payment without PMI. FHA timeshare new orleans cancellation is presently the go-to program for home buyers who may not certify for standard loans. Fortunately is that you will get a similar rate or perhaps lower with an FHA home mortgage loan than you would with a standard one.

Not known Incorrect Statements About What Are Interest Rates Today On Mortgages

According to loan software company Ellie Mae, which processes more than 3 million loans per year, FHA loan rates averaged 3 (what does ltv mean in mortgages). 01% in October, matching the typical conventional rate. Another intriguing stat from Ellie Mae: About 20 percent of all FHA loans are provided to candidates with credit rating listed below 650.